Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv U.S. House of Representatives CSPAN January 7, 2010 10:00am-1:00pm EST

10:00 am

of options available to you. if you have no insurance or access to insurance through an employer. it feels like, yes, in order to have reform, there are new rules for government, and new rules to get rid of preexisting conditions, which means enforcement of those rules. then we had a substantial number of programs trying to improve, for example, health care statistics. we don't have timely information on what the costs we are, we do not know county by county how well we're doing with pneumoniae and surgical complications and that kind of information has to be more readily available. although i am pretty much in agreement that creating more government is a place where we can find ourselves hamstrung by bureaucracy, at the same time,

10:01 am

we are in a place where the leading the system to itself -- where leaving the system to itself, we are watching it collapse, people ought not only by a lack of care, but even -- people harmed not only by lack of care, but disorganized control of care. host: thank you for spending time with this is an audience. and thank you for joining us. we will be with you again tomorrow 7:00 a.m. eastern time. until then, have a good day. [captioning performed by national captioning institute] [captions copyright national cable satellite corp. 2010] .

10:02 am

elsewhere in washington, a discussion on u.s. policy toward afghanistan and pakistan. richard holbrooke will be at the parking institution today to talk about the obama administration policy. but coverage at 2:30 eastern. we will be joined by tomah vilsack for everything at the

10:03 am

state department. in his -- for a briefing at the state department. >> the new c-span video library is a digital archive of c-span programming from barack obama to ronald reagan and everyone in between. over 157,000 hours now available to you. it is fast and free. try it out. >> vice chair of the federal reserve and economist martin feldstein at the meeting in atlanta. they will talk about the economic policies of the first year of the obama administration. this is just over two hours. >> good morning.

10:04 am

>> this is the andrew brimmer 81.his forum this forum was organized in the spring of 2008. the forum itself will start in boston in the year 2000 and since that time the association has been good a enough to allow me to sponsor this forum every year since so this is the 11th occasion. >> is very light on here?

10:05 am

>> this year's forum was titled the national economic policies of president juan barack obama evaluation after one year on the trail. the speakers in the book will appear the order in which they are listed in the book except a few days ago dr. christina romer sent me a nutter seeing the work of the council of economic advisers and the president's message economic reports and so on she could not possibly come to atlanta today. so, she instead asked whether alan krueger assistant secretary of the treasury and the chief

10:06 am

economist was coming to the matter and he would be prepared to make a presentation who stands, so allen is here and i'm grateful to him. we have one technical problem. she has a powerpoint presentation. i told him at the time when we talked at my assistant, henry, would be here, because at the time i thought i would have a power point presentation and that she would be willing to substitute -- to preserve him as well. unfortunately she's not here yet. [laughter] but she is in the building -- >> she's here. [laughter] >> thank you. i'm sorry.

10:07 am

i'm sorry. you need to have a word with allen. [laughter] please allow loss to do this. i think his presentation would be much more efficient if we could do it this way. in the meantime, you can look at me. [laughter] well, i should say the program outline is suggested. the presenters were free to do whatever they wished. the content is their own, and they are prepared to proceed forward.

10:08 am

>> -- [inaudible] >> all right. then let us do that. the vice chairman of the federal reserve board. >> thank you, and i'm very pleased to be able to participate in this year's brimmer's policy forum. governor brimmer and i did not overlap at the board, but i admired his work from the bank of kansas city where i started my career in 1970 and my colleagues in the federal reserve and i have greatly benefited since then since his analytical approach to different public policy issues. this morning i thought it might be useful for me to review the course of monetary policy through the crisis and highlight a few issues for policy for the future and i would like to start

10:09 am

with an important clarification. first, despite the title for what i am about to discuss is and president obama's monetary policy. it is the federal reserve's. [laughter] fortunately, the administration has been careful to respect the independence of the federal reserve and the conduct of monetary policy. it recognizes that the federal reserve insulation from short-term political pressures is essential for fostering achievement and its legislative objectives of stable prices and maximum employment overtime and the second important clarification is the views you are about to here are my own and not necessarily those of any other member of the federal open market committee. let me start with monetary policy path. i have a past, present, future kind of presentation here. as it related to discussing where we are now and issues for the future i thought it would be helpful to summarize the actions we took over the past two years.

10:10 am

in august, 2007 we recognized we were coping with a potentially serious disruption and financial markets that could feedback adversely on the economy and job creation. with liquidity and key funding markets drying up some markets closing down, policy interest rates alone for maudlin to be enough to keep financial conditions from tightening severely for households and businesses. our first actions were to ease the access of depository institutions to federal reserve liquidity. but as the crisis worsened it became apparent that these actions along with being sufficient. securities markets had come to play a prominent role in channeling credit in our economy, severe disruptions outside the u.s. banking sector were threatening to reduce economic activity. to counter the financial stocks

10:11 am

hitting the economy and support the flow of credit to households and businesses, they they needed to extend liquidity to support a range of mom bank institutions and some financial markets. as we expanded the reach of our liquidity facilities, we generally followed the time-honored central bank behavior in a crisis. extend credit freely to solvent institutions at a penalty rate against adequate collateral. by making liquidity available more broadly we are trying to break the vicious spiral of uncertainty and fear feeding back on asset values and credit availability and from then back to the economy. we also found we need to innovate by making liquidity available through auctions as well as standing facilities to overcome reluctance to borrow from the federal reserve out of concern the borrowing could be inferred by market participants and viewed as a sign of

10:12 am

weakness. in view of the likelihood financial developments would lead to the weakening of aggregate demand we began to lower the federal fund rate in september of 2007 well before any hard evidence had become available regarding the magnitude of the restraint it might impose on economic activity. as it became increasingly evident over the course of 2008 that the financial disruptions were sending the u.s. economy into recession we picked up the pace of reductions in the fund target. importantly, our ability to move aggressively was enhanced by an environment of already low inflation and stable inflation expectations. to ease financial conditions further, even after our policy interest rates have approached zero, we needed to operate directly on longer-term segments of the financial markets. even though various types of debt securities are typically

10:13 am

quite substitute double our purchases of agency guaranteed mortgage-backed securities and agency debt and treasury securities evidently we are successful in reducing the long term interest rates partly because during the crisis private-sector participants had a very marked preference for short-term assets. and this highly unusual such region and with the normal response of monetary policy interest rates constrained by the zero low were bound we considered it especially important we convey as clearly as possible our policy intentions to the market participants as they formulate their own expectations for the future path of interest rates and help in this regard we have noted in the statements we have released at the conclusion of each fomc meeting our expectations of exceptionally low rates will likely be warranted for an extended period. keeping inflation expectations incurred is always important but especially so in the current

10:14 am

circumstances given the potential effect of the unprecedented economic developments and policy actions of the past two years on households and business views on the price outlook and to provide more information to the public about our own expectations and objectives we have extended the horizon of public projections of fomc participants to five years, supplement these projections by reporting a long-term inflation rates, committee participants viewed as most consistent with satisfying our dual mandate. in the absence of any other government agency having the authority to fill the role we have led to stabilize several systemically important institutions any one of which had it failed to have posed a serious threat to the financial system and the economy. these actions was necessary or not well-suited for a central bank and we have urged the congress to enact other means of

10:15 am

safeguarding financial stability in such circumstances while imposing cost on shareholders management and whenever possible creditors. financial our kids are performing much better now than they were in the early 219. our liquidity facilities, the reduction of uncertainty about the capitol liquidity needs in@r barrowing from the federal reserve has dropped dramatically. in addition, many securitization markets appear to be functioning more normally. partly responded to the support we provide in the talf facility. as we affirmed at the meeting, the federal reserve is in the process of winding down and closing most of our

10:16 am

extraordinary liquidity lenders. wn and closing most of our extraordinary liquidity windows. our announcements of purchases of agency and treasury securities helped lower long-term interest rates and increased availability of mortgages to households and bond financing to businesses. in addition our mere zero policy read and improving economic outlook have induced shift by private investors into longer-term and riskier assets helping reverse a portion of the previous spike in spriggs that occurred as the financial economy and financial audits deteriorated. with markets improving the economy expanding the fomc has also indicated that we are to bring down our purchases of treasury, and bs and agency securities. but the cost of credit remains relatively high and its availability relatively limited for many borrowers.

10:17 am

although many long-term interest rates are fairly low spreads and markets are somewhat elevated not surprisingly perhaps as many borrowers are still under stress with unemployment rate quite high and utilization to capital stock still very low. some securitization markets continue to be effectively closed or severely impaired including those for larger home mortgages and commercial real-estate loans. under these circumstances, some borrowers will be more dependent than in the past on banks for credit but banks are still reluctant and very cautious lenders. banks have been reducing their book of loans for about a year. in part this reflects weaker demand as businesses cut back on inventories, households have been saving more. but the weakness in the bank lending also results from cutbacks from supply. our surveys show through late

10:18 am

2009, banks continue to tighten terms and standards for lending and to raise rates they charge relative to the benchmark rates. i expect bank credit to turnaround only slowly as banks rebuild capital and become less on certain about economic prospects. wondering how credit constraints or a key reason why i expect the strengthening and economic activity to be credible and the drop in the unemployment rate to be slow. even as the impetus for fiscal policy and inventory cycle weems leader in 2010 however, private final demand should be bolstered by further improvements in securities markets and gradual pickup and credit availability from banks. in addition, spending on houses, consumer durables and capital equipment should rebound from what appear to be exceptionally low levels and we've already seen some hints of this increase in private demand in recent months. but understandably, households

10:19 am

and businesses, bank lenders remain very cautious, and the odds are the pickup in spending will not be very sharp. in an environment of considerable persisting slack and labour and product markets with productivity having increase substantially in recent quarters, cost and price inflation should remain quite subdued. in the shortest run headline inflation will be driven importantly by movements in energy and food prices but judging from the structure of the future crisis markets are not expecting sharp rises in the prices and thus headline inflation should retreat toward the core inflation. inflation now side of the food and energy sector that is core inflation has been declining slowly held up by relatively stable inflation expectations. some further slowing is possible if the economic rebound is as gradual as i think it is likely to be. as i've already know to keeping

10:20 am

inflation expectations incurred will be critical for achieving our objectives in prices and output. fomc has recently reiterated its expectation of the considerable remaning slack and labour and product markets subdued trends and inflation expectations are likely to warrant exceptionally low levels of the federal fund rate for an extended period. let me turn to two issues for the future monetary policy. the first one is exit from our unusual policies. i'm not going to discuss the technical aspects of an exit from our extraordinary measures. federal reserve cut the public a price of the development of our exit tools, appropriate use and sequencing of the tools is still under active discussion by the fomc but i do want to make some general strategic points about its. first, we have no shortage of

10:21 am

tools for firming the stance of policy and we will be able to unwind our actions when and as appropriate. because we can now pay interest on excess reserves and raise short-term interest rates even with an extraordinarily large body in reserve in the banking system. increasing the rate we offered to banks on deposits of the federal reserve will put upward pressure on all short-term rates. in addition, we are developing and testing techniques for training of large volumes of reserves through repurchase agreements and through term deposits at the federal reserve. and we can sell portions of our holdings of the nds agency debt and treasury securities if we determine doing so is an appropriate approach to tightening financial conditions when the time comes. second, the fiscal situation will not impede timely tightening. the trajectory of the federal budget is a serious economic issue that must be addressed to

10:22 am

promote sustained and balanced economic growth. but a large and growing federal deficit will not stop the federal reserve from accepting from current policies when that is needed to keep prices stable. and the economy on a path to sustain high employment. the alternative of letting inflation rise would be inconsistent with our mandate and would only cause greater volatility, uncertainty and inefficiencies that would reduce the growth of our economy over time. ho your interest rates could complicate an already difficult fiscal trajectory. and this possibility further underscores the critical importance of maintaining federal reserve independence in the short term political pressures. faired because monetary policy typically acts with long-term rags on the economy and price level of when and how to exit will depend on forecast.

10:23 am

we will need to begin withdrawing extraordinary monetary stimulus will be for the economy returns to high levels of resource utilization. the fomc has been clear that its expectations from the stance of policy depend on economic conditions including resource utilization, inflation and inflation expectations. the judgment as to when to begin a initiating steps to withdraw stimulus will in turn determine these variables. finally it is well to remember that we are still in on chartered waters. we do not have any recent experience with financial disruptions of the bread, persistence and consequences of those we experienced over the past several years and we have no experience with most of the sorts of actions the federal reserve has taken to counter the shock. the calibration of our exit from these policies is complicated by

10:24 am

evidence on how unconventional policies work. we will need to be flexible and adjust as we gain experience. second topic for the future, financial stability and asset prices and monetary policy. the past few years have illustrated to lessons about the relationship between macroeconomic stability and financial stability. first, macroeconomic stability does not guarantee financial stability. indeed in some circumstances macroeconomic stability may foster financial instability lowering people into complacency about risk. and second, some shock to the financial system are so substantial especially when the weekend large number of intermediaries that decrease in aggregate demand can be a large, long lasting and not quickly or easily remedied by conventional monetary policy. so, given the heavy costs that

10:25 am

have resulted from the financial crisis, the question naturally arises whether the circumstances that caused the crisis could have been avoided. among other crucial policy issues, we need to reexamine with open mind whether conventional monetary policy should be used in the future to address developing financial imbalances as well as the traditional medium term macroeconomic goals of full employment and price stability. the key question is whether we are likely to know enough about asset price misalignment and like the effective policy adjustments to give the confidence to deliberately tack away for a time from the exclusive pursuit of the posturing eckert price stability and high on employment. obviously, preventing situations like the current one would be very beneficial. but against this important objective, we need to balance the potential costs and uncertainties associated with

10:26 am

using monetary policy for that purpose. especially in light of the difficulty in judging the appropriateness of asset valuations. one type of cost of arises because monetary policy is a blunt instrument to. increases in interest rates stand activity across a wide variety of sectors. many of which may not be experiencing specter but activity. moreover, monetary policy generally operates with one instrument, short-term interest rate, and using it to dampened asset price movements implies more medium-term variability in output and inflation are around their objectives. among other things inflation expectations could become less well anchored, diminishing the ability of the central bank to counter economic fluctuations. in the current situation output expected to be well below its potential for some time and inflation likely to be under the 2% level that many fomc

10:27 am

participants see as desired over the long run. tightening the policy to head off a perceived threat of asset price misalignment could be expensive in terms of medium-term economic stability. furthermore, small policy adjustments may not be very effective in reading and speaking to the excesses. our experience in 1999 and in 2005 was that even substantial increases in interest rates did not seem to have an affect on the dot com speculation and first instance on housing price increases in the second. larger adjustments would incur greater in incremental cost. policy adjustments need to dampen the speculation. if higher interest rates just a week in the output and inflation without dampening the speculation, the economy could be more vulnerable when the speculative bubble bursts. we do not have a good theories or empirical evidence to guide policy makers and their efforts

10:28 am

to yours short-term interest rates to the financial speculation. for all of these reasons, my strong preference would be to use regulation and supervision to strengthen the financial system and lean against developing problems. given our current state of knowledge monetary policy would only be used if in balances were building and regulatory policies were either unavailable or shown to be ineffective. but of course we should all be working to improve our state of knowledge so as to better understand economic and financial behavior and further expand the range of policy tools that can be employed to enhance macroeconomic performance. that objective is one that governor brimmer has worked very hard to promote. thank you. >> thank you very much. [applause]

10:29 am

>> [inaudible conversations] >> i apologize for the technical difficulties. i also think and brouhahank andg me to substitute for christina

10:30 am

romer. i did not ask her the subject. i did ask her what message with she would like to deliver here in she said please explain the actions the administration is taking to combat the problems in the economy and that they are working. [laughter] i take that as my theme. and i also tend to agree with her observation that they're working. i will explain why. the economy was in a free fall back in the end of 2008, early 2009. financial markets had frozen up. private demand was collapsing. employment was plummeting. we were losing 700,000 jobs in the first quarter of 2009. home sales were falling sharply. and the economy began to stabilize around late spring. this was the time when chairman

10:31 am

bernanke mentioned the green shoots. since then, the financial markets stresses have eased, housing markets have shown signs of stabilizing, dgdp has moved higher. higher, 2.2%, gdp growth in the third quarter after four consecutive quarters of decline drops five, 6% at the turn of the year at an annual rate and employment losses have also shrunk considerably. there is still much to do. i have said when the employment report comes out less that is not good enough. the unemployment rate is unacceptably high at 10%. but the economy appears to be on the road to recovery and that is because of the actions the administration has taken. i don't mean to diminish the role of the fed the session is on the administration's actions.

10:32 am

and the president is committed to building a stronger foundation going forward including health care reform. in absolute terms however the economy still remains weak. gdp is 2.6% lower than it was a year ago. at least it was at the third quarter. i will argue the policy has prevented an even much worse about comes and the three policies on will highlight and i think they work together or the financial stabilization plan, housing policy and the stimulus bill. the american recovery reinvestment act. and to assess the track record of the administration in the first year, i think it's very important to compare to a counterfactual to how the economy would have behaved absent the policy actions that were taken. there's a quote from barney frank of like which probably many of you have heard but i thought i would read. congressman frank said not for the first time as an elected official i envy economists.

10:33 am

economists have available to them and an analytical approach to counterfactual. economists can explain a given decision was the best one that could be made because it can show what would have happened in the counterfactual situation. they can contrast what happened to what would have happened. no one has ever gotten reelected with a bumper sticker that said it would have been worse without me. [laughter] you probably can get tenure that way that you can't win office. [laughter] now i guess there are two respects i disagree with. first it is not always so easy to construct a counterfactual although we make some arguments about the counterfactual obligation. and secondly i think my colleagues, tama has a paper that shows they are going to be reelected of the situation is worse in the neighboring states, so i would argue the count effect will this matter even in elected office. so i want to highlight the

10:34 am

financial market policies, and i will focus on the stress tests here. but there is more to the financial market policies of the administration than the stress test. but the stress test officially known as the supervisory capital assessment program which was administered by the federal reserve and other banking regulators and announced by treasury secretary geithner on february 10th was designed to assist the capitol needs of the bank's in an adverse economic scenario to be as transparent and clear as possible to make the information available so investors in the public can see the situation of the banks and also very importantly the treasury's stood necessary with the capital assistance program to provide government capital if there was inadequate private sector capital. now the counterfactual situation here is hard to assess the level to highlight something that my

10:35 am

colleague paul krugman wrote in "the new york times" back in february before the stress tests were concluded. to in the buzz on the hood the banks need more capital. but they can't raise more capital from private investors. and i think the conventional wisdom before the stress tests were announced in may of 2009 was the banks would not be able to raise private sector capital in fact paul krugman wrote in less than seven columns proposing we nationalize some of the bank's. since the stress tests were released, banks have raised the total of $150 billion in equity and issued over $64 billion in guaranteed debt. if you look at this chart shows month by month the net issuance of common equity by banks call and you can see that in the second quarter when the stress tests were released we see the reversal here from declining equity which means buybacks to issuance of capital.

10:36 am

this next chart shows you the capitol levels of banks, the ratio of tangible common equity to assets for the stress tested banks the 19 largest banks that went through the stress test the account for two-thirds of all lending in the u.s. and you can see a sudden reversal in the level of capital in the bank's. and it was a rather dramatic turnaround. you could also see this looking at the credit-default swaps for banks. the cds spreads are an indication of the likely the banks will default. this looks of the largest banks because that's the group you can get continuous cds the debt and you can see after the failure of lehman brothers cts spread shot up and when the stress tests were released there was a discreet drop in the cbs spreads. this stress tested banks.

10:37 am

when i do econometrics i call this an intricate series that you can think of the counterfactual it is a very sharp discrete event that happened on may 7th of 2009 when the stress tests were released. this chart shows just for citigroup. and i wanted to show citigroup because as you know citigroup has repaid tarp funds and this shows the fall even after the period it paid back its t.a.r.p. funds. now there's a lot more to the financial stability stabilization plan. the administration of the t.a.r.p. program is obviously a big part of it. i don't know how widely known is that for the banking successor to beat considers a whole the t.a.r.p. investments payback for the taxpayer were projecting that will make a profit from the taxpayer from the investments in

10:38 am

the banking sector. other stress as don kkohn mentioned our market and, many are to the pre-christmas level, some are partly back. the index is back at low levels. municipal bond spreads, the municipal bond market had frozen back in the end of 2008, early 20093 that market is not functioning and on the spreads are close to normal. so there is a lot of indication that the financial markets have stabilized. president obama was asked for his most important achievement of 2009 and he said that we prevented the financial market from collapse sterilizing the financial target's i think was an important achievement of the administration and it wouldn't have happened absent policies of the obama administration and federal reserve board.

10:39 am

let me turn to the housing market. as you know an important cause of the crisis we are in was a bubble in the housing markets. the administration has taken several actions to address housing market problems. one approach is to lower mortgage rates and increase access to credit. this involves continued control of the gse of fannie mae and freddie mac providing access to the sustainable mortgages through the fha federal housing administration. treasury as well as federal reserve board purchases of mortgage backed securities and a program, part of the making home affordable program which increased flexibility for home refinancing. and all of this has led to lower interest rates as well as three high volume of refinancing activity. second, the administration has

10:40 am

sought to make it affordable for people to stay in their homes. the research suggests that for someone to walk away from home you need to things, one for the house to be underwater and secondly the payment to be unaffordable and that is typically required just for defaults. the administration focused on making it affordable for people who are responsible homeowners to stay in their homes. we have the goal of supporting three to 4 million homeowners to modify their mortgages to lower their payments. so far over three-quarters of the million homeowners have modified their mortgages under this program. this is a program which gets a tremendous amount of criticism in the press and i think it is an indication of the cynicism in the press come partly an indication of some of the difficulties of getting it very large program started. but if you think that this is a program that started at the end of march, early april and we

10:41 am

were originally criticized for not doing enough trial modifications, the home owner has to be in a trial period for three to five months before they can convert to a permanent modification, and the program started slowly as we were signing of servicers as they were putting in place procedures to get the program running. but now we are actually ahead of schedule and my office did much of the budget scoring for this program. we are actually ahead of what we predicted to make the three to 4 million target in terms of starting modifications over 750,000 so far were in and 2009. the latest wave of criticism, which i think is justified although i think it addresses problems we will eventually see fixed is too few of the trial modifications are converting to permanent status. just under 10% of the eligible to file modifications have converted to permanent status.

10:42 am

now, partly that is also getting the systems in place reducing uncertainty. problems with filing paperwork and so on and anyhow we are not satisfied with the speed of which the trial modifications are converting to private, to permanent modifications. on the other hand, we are addressing these problems and i think we will see improvement in this area. and it's also the case the homeowner is undergoing trial modifications are saving substantial sums while they are in this three to five months period which file modification sitting around $550 a month on average. then the last component is the first-time homebuyer credit which was just extended in 2010 by the congress. so one way to kind of get a handle on how the housing market is staring and responding to these policies is to use the future market as a kind of counterfactual.

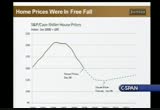

10:43 am

what were markets predicting for home prices back in january of 20 online before these policies were put in place. this shows you the case schiller house price index and you can see the home price bubble i mentioned earlier. next the negative line here shows that from january 21 line with the radar what futures market was projecting for the home price is almost another 20% drop in home prices are being projected back in january 29 a year ago. what happened since then -- by the way, i should mention the radar futures market is kind of a thin market. nonetheless, you know, it is less than one econometric projection it also those are participating in the market have money on the line so there is some reason to think this might provide plausible counterfactual scenario. what happened since then, as bond kkohn mentioned earlier, as

10:44 am

house prices has stabilized even increased a little bit. the futures market are now projecting flat line for the next few years. so, i'm going to be very careful not to say we are out of the woods in the housing market. the housing market remains very fragile. on the other hand, there are indications the market is stabilizing faster than a lot of the observers had expected. and then other measures of the housing market are also beginning to stabilize like the inventory of homes for sale. the last leg of the school that i mentioned is the recovery act. the recovery act as you know is a 787 billion-dollar program designed to fill in for much of the shortfall in the private demand due to the deep recession. there are three main components, tax cuts come support for infrastructure, and then support

10:45 am

to vulnerable populations by raising this shouows q that the taxes ae multifaceted. they are also tax subsidies under the unemployment program. there are many projections of the effect of the stimulus bill on jobs. how many additional jobs would have been lost absent the economic activity generated by the stimulus bill. they are all in the range of 1 million jobs so far. a kind of of the best looking copper -- a kind of honest way at looking at the projections. what i did projecting for gdp

10:46 am

growth? of the shows the average forecast for the blue-chip forecasters each month. you can see that back in april the projection was around 1.5% gdp growth and now it is close to 3%. 1.5% gdp growth for the fourth quarter and not a projection as close to 3% for gdp growth in the next couple of months. but you can see that forecasters are raising the projections use all the same thing in the third quarter and i don't think that is an accident. i think it is the result of economic policy pursued by the administration and federal reserve board. so let me conclude by saying the president said on many occasions that rescuing the economy from the deep recession is not sufficient. we need to rebuild the economy and put it on sound footing. an important component of that

10:47 am

is health care reform, the congress is on the verge of passing historic health care reform. in addition the administration is pursuing financial regulatory reform. also because jobs have been lagging and jobs tend to lag in recovery the administration has been working with congress to try to develop proposals to emphasize job growth and spur job growth in 2010. and then lastly i will just emphasize the set of problems the administration inherited were tremendous, including the large deficit due to the tax cuts that were not paid for and prescription drug program not paid for. the president is committed to putting the federal budget on a sustainable path when the budget for 2011 is released and projections and policies going forward. the ad penetration is committed to putting the u.s. to run it on a path toward fiscal stability.

10:48 am

thank you. [applause] >> allen sinai. >> while allen is standing up copies participated in virtually all of these since the year 2000. allen sinai >> thank you for inviting me this year and the other years. it is a pleasure to participate. the work i did for this session -- we did, paul adelstein senior economist at the company myself, it spans both administrations and it's all about policy, not about politics, and so any grades anybody might infer from the work here has to do with the effect of policy on the economy during the 2007 to 2009 period.

10:49 am

and what we have today and you have a handout of tables and charts is an abbreviated version of the paper and key results from retrospective counterfactual simulations with a large scale quarterly macroeconomic model. the following question is asked what would have happened to the economy, employment and unemployment rate, inflation and profits, interest rates and stock prices, some of the tables covered that much territory. from 2007 to 2009, the period that we could call a great recession if the fiscal monetary policy actually implemented had not been implemented. since actual historic data have invaded and in the policies actually implemented at least so far removing them from the model

10:50 am

base version of history that tracks closely the historical data pulled the baseline allows the economy eckert model or any other model that might be used for such a purpose to simulate what history would have been without the policies. counter the actual analysis and simulation have long been used although not frequently in modeling and in the evaluation of policy. lately in what i think is the path breaking attempt by john tayler mittal logically to evaluate the current policies especially monetary in real time at the inaugural martin feldstein address this past july. in the attempt to determine at the time if policies are having any negative will affect in order to alter them sooner if they are not effective i think is of immense mythological

10:51 am

significance for policy evaluation a practice. most contracts also malaysians have been performed long after the fact as was noted by john including one on i did back in 2004 in the may issue of the american economic review of the need for preemption and monetary policy and leaving the lives generally. the conclusion of virtually complete ineffectiveness and that is relevant for today's session. the complete effectiveness of monetary policy as it had been taken, and for the fiscal policies being used it is not supported by the empirical results of the large scale counterfactual work that we did. john's underlining model is very different with much in common but with many omitted variables and less structural content and underscore is that any counterfactual simulations are very model specific.

10:52 am

if you believe the model you will be persuaded by the results. of course i believe our model is a rather complete representation for the macroeconomy and financial system, and therefore i am quite comfortable with its results though i would emphasize the mythological point of the tayler exercises has huge implications for policy analysis that is doing it right away as but even as our obering rather than waiting a long time. now the work is fairly quick. we are not through the effect of the policies that we have retrospectively simulated. the effects are still playing out. so, it isn't quite real á%@@ @ a the work covered the history 2007 to 2009 but extended in

10:53 am

simulations through 2012. the base line had actual history up to the fourth quarter of 2009, but have a forecast baseline out to 2012. in the baseline track history would have the prospect in a fairly mainstream view of the economy over the next few years. a fairly view of the economy over the next few years. let me take you to the tables and figures in the handout for a quick survey of the highlights. but before i do that and we use some of the tables to illustrate the point was there a great recession i think if we look at table number one in the handout

10:54 am

and in particular the three-quarters bounded by the black lines and the wide number of countries in global regions covered i think 46 or 47 we see is something never seen in the post-world war two history in the u.s. and the world and incredible kind of cliff like collapse of economic growth in the u.s. and around the world concentrated in those quarters. some extend beyond to the second quarter of 2009 and in some started before the bout of period the point of this table is the incredible and stunning downturn around the world that went on during this purpose of time. by the way for the u.s. table

10:55 am

number two is a guess at the dating of the last recession. september or october. can't read the mind of the national dating committee but this is a guess, the downturn in the united states was the longest 23 months at best 22, the worst 24 and deepest since world war ii but the deepest for this episode is in parentheses if you take the trough as the second quarter last negative quarter of real gdp gdp is 3.7% which is any decline from peak to trough since world war ii. this was the longest in the u.s. and the deepest downturn that we ever had. now why? it's complicated. lots of things happen that went

10:56 am

on. but i would isolate for purposes here a couple of major facets which are not adequate to describe the complicated interactions that went on in this downturn on like virtually any other business cycle that i have ever seen and studied. table three provide the kernel of thought. it's the financial factor in business cycle and this time and unusually so the american consumer in table three you see two asset-price bubbles bursting in the climb of real estate prices and stock prices over the great recession pro.

10:57 am

uncomfortable because if you look at these numbers it was the biggest recession. it's a great recessions i'm going to call it that. now you see also the effect on household wealth, household net worth, the biggest declines. of course because of the declines in real estate and stock values of assets in the period chronicle since 1947. in figure one or two sources of household spending financially driven gross cash shouts from refinancing and individual capital gains realizations which in our work on consumption and the consumption function is very sycophant quantitatively. and it plummeted over the probe of the great recession.

10:58 am

the impact on consumer spending of these to their labels and in addition to standard variables like wells, interest rates and real income is quite significant into wrigley. 25 cents on the dollar of capital gains realizations. 30 cents on the dollar within the year of the gross refinancing that came off the mortgage and housing boom that's gone up and of course the sources of funds for the household consumption were devastated. and in figure two we see how the measure we used for the financial condition of housing sector high levels are bad, low levels are good. and what you see over the 2007 to the 2009 period just now peaking here at about this time in the second and third quarter starting to come down is the most dtv financial position of the house will sector since

10:59 am

we've been keeping this since 1970. the sign that imbalances, excesses' had built up over the period and consumers have a long way to go to fix that. and then figure three the role of the american consumer demand by the way this figure shows the same thing in real per-capita terms as it shows here. the longest period of consumption spending growing below trend of any time and including 1973, 75 and putting the early 1950's and still going we've been returning to trend 70% of gdp related to the financial factor from the charts and tables had changed before. when you have a change in the growth rate at the spending

11:00 am

aggregate, that is a portion of the economy. it is different from history. multiplier accelerator effects are going to kick in and reverberate everywhere. in fact, in this case, all around the world, because as you know, the american consumer was a huge buyer of exports from lots of countries. that went away. it levered those economies. these internal reverberated back to the united states. of all the things that went on, including the subprime problem, if i had to isolate two things, it would be the financial sector in the business cycle -- and the business cycle.

11:01 am

the negative feedback loop bacb to the economy. those aspects of this particular cycle that had so much to do with the intensity of the downturn. . . cycle that had so much to do with the intensity of the downturn. now what about the reactions of the policymakers to this? i think i would have to say as i have always said in observing policymaking with regard to the ideal situation in the economy and what we can create and a test tube in macroeconomic policies to get what we should get in terms of the objectives and the timing you know frankly that is impossible in the practical world of policymaking because too many things

11:02 am

interfere with that. what he can do we cannot do in what he can do we cannot do in the laboratory of the feder policy makers. i think once recognized leader in 2007 by the federal reserve and the congress and the bush administration and in the obama administration 2008, 2001 policy actions were taken fast and furious and we've heard about that from allen already today. and in the too late, too slow, too timidly and arguably fiscal policy perhaps the wrong mix with the wrong proportions. certainly t.a.r.p. in some timber, 2008 in my opinion was way off in terms of what one could have done with the taxpayer money and i must say the evolution of how t.a.r.p. ended up being used is more encouraging, but this was one of the worst examples of the public policy in eight macrosense that i think i've ever seen it all

11:03 am

the years i've been looking at this and this is a topic for another day. for the policies and tables for and five and into gear for you see what we call the monetary policy easing or the monetary policy response. .. >> these characteristics of policy have significantly

11:04 am

different because of the way the model reacts but it is these policies and their major elephants need -- elements. excessing the effects of the- household balance sheet that happened. you can at your leisure look at the tables that show the changes to a number of major hurdles as a consequence of taking out the policies directly and collectively. singly, jointly, and collectively. what i want to concentrate on for a minute or two as table 16 in figure 13, which provide a comparative summary of these counterfactual simulation.

11:05 am

and in them, what we see are some conclusions that i would draw. first, it is clear that collectively the fiscal and monetary stimulus made a big difference to economic performance in 2009 and will in 2010. a much worse result would've occurred if nothing had been done. over two percentage points less real economic growth in 2009 and in 2010 more than four percentage worse economic growth than is currently expected is what these counterfactual simulations show would've happened without any of the allah sees, and none of them being implemented. we would have had economic growth of four to 5% this past year and 82,000 down of 2% without any of these policies. also, quite clear both in history and in the business cycle again is the timing of policy making actions.

11:06 am

way too slow, not preemptive enough, and probably for the short term not adequately sizable. again, this is idealism talking in the laboratory as opposed to the practical side of policymaking with which i am familiar and the difficulties of doing things on time and early enough. between the various policies the results show much greater effect for the monetary you seem for the fiscal stimulus. you can see this in the summary table monetary policy 16, monetary policies in both reductions of interest-rate and quantitative using if not implemented would've cost about two percentage points of lost growth in 2009 andover three percentage points in 2010. monetary policy is powerful although with flags. the fiscal policy stimulus boasts to non-recovery act in the 2008 in the obama administration to pass nine if not implemented would've cost

11:07 am

the economy over half a percentage point of growth in 2009 and 1.3 percentage points in 2010. the monetary policy is clearly far more significant and within the monetary policy easing it is quite interesting that our model verdict is that the quantitative easing had much bigger impact than the interest-rate reduction in the federal funds rate. the quantitative easing, the ingenious invention never seen before in the history of macro policy in the united states of this federal reserve and i must give them a lot of credit for figuring and trying all that stuff. the model tells you that. now why the model is saying that we have to take a real good look at, but it is definitely quite clear about that. on the fiscal side,@@@@@@@ @ rdz

11:08 am

>> i listened to don, i listen to allen. the dam and comments to the federal reserve were quite appropriate and i would suggest that you continue to do that. thank you very much. would suggest these results that you continue to do that. thank you very much. [applause] >> marty? >> randy, thank you very much for providing inviting me to participate in this and i'm grateful to you for organizing

11:09 am

this forum year after year and it's a pleasure to participate with everyone on the panel. i'm going to talk about three topics. i'm going to start by talking about the use of fiscal policy as a countercyclical instrument. i then want to say a little bit about fiscal deficit and then finally i want to talk about what was the key fiscal economic policy of the past year in my judgment. and that is the health insurance legislation. so i'll start with a countercyclical instrument. this really has been a different business cycle for previous business cycles. we look at previous economic downturns that were caused by a tightening of the federal funds rate, the fed tightened because it was concerned about inflation either actual or incipient inflation. and when it had succeeded in doing what he set out to do a good lower the short-term

11:10 am

increased rate the economy could recover. and that typically took about from pete to trough. in a key part of the recovery with the bounce back in housing interest spending on housing. this time the downturn was not caused by federal reserve tightening. it was caused, i think if you have to summarize it briefly, by a miss pricing of risk and as a result of that miss pricing of risk excessive leverage and that in turn led to affect a bold. and when the asset bubbles broke, the economy turned down and allen sinai has given us an explicit focus on the two key asset bubbles that contributed to the decline in household spending. but once that happened, monetary policy of the traditional lowering interest rates was simply not affect this.

11:11 am

the banking system, the capital markets more generally were dysfunctional. housing was certainly not going to respond to one or two or three percentage point reduction when house prices were coming down at 10% a year. so, the fed changed the direction because the fed became a provider of credit and really stepped in to replace the dysfunctional private credit markets. that's not my subject for today, but i think it's important to see the ineffectiveness of traditional monetary policy in being able to generate a recovery as the rationale for the fiscal policy. i reluctantly came to that conclusion in the summer of 2008 that we needed a significant fiscal stimulus.

11:12 am

usually fiscal policy is a bad choice. it's a bad choice because the lives ourselves on. but this time in contrast to the traditional ten-month peak to trough history this time the lag was clearly going to be a lot longer and on top of that monetary policy was ineffective. so i supported the idea that we needed to have a fiscal stimulus summer to the dismay of some of my conservative friends. i advocated in any article in october of 2008 in the "washington post" that whoever was going to win the election the next month was still going to be a senator whether it was mccain or obama and that they should move immediately to develop a fiscal policy instead of waiting until the spring of

11:13 am

2009. well, president obama did weight. in fact he stepped out of the assignment immediately after winning the election. moreover he returns the responsibility for designing that fiscal stimulus to the congress. and i think that in richer spec was a serious mistake. the result was that we had a 787 billion-dollar plan which delivered much less stimulus, much less increase in gdp, much less improvement in employment then $787 billion should have. too much of it went into transfers, into payments for states to finance further transfers by the states and to protect public sector jobs. it was a low multiplier use of funds. nevertheless, it did work as

11:14 am

alan krueger said. it worked in a sense and we thought now and finite numbers at the gdp has been better in the past couple of quarters than it otherwise would have. but what i would emphasize is that it was a low-cost affect admits policy. we got a small increase in demand and if we take that 1 million increase in the number of jobs would early while fiscal policy did embrace the gdp, while the fiscal stimulus was expanding, it went from nothing in the first quarter to roughly a $40 billion fiscal stimulus in the second quarter, and then more than double that in the third quarter. it was annexed -- it was expanding at an important rate.

11:15 am

while that happened, we saw gdp rising. the question is, what is going to happen going forward? in 2010, the level of the fiscal stimulus is stable, no longer rising. it is very, is stable, but it is no longer rising. take some of the negative forces that we still see in the economy and we saw in the third quarter. it is the declines in the state and local government spending. if the declines in the business fixed investment continue and we do not have an offsetting targeted thrust from an expanding fiscal stimulus, will the economy continued to expand throughout 2010? ued to expand throughout 2010? and i think the answer to that is still unclear.

11:16 am

we don't know what's going to happen. i think there is a significant risk that the economy could run out of steam at some point in 2010. and that we could see a further downturn. what is clear is that $800 billion was added to the national debt. maybe some part of that was offset to the extent that we got more gdp. we got more tax revenue. but it was an enormous increase in the national debt. so that brings me to my second topic, which is what to do about fiscal deficits in the coming decade. and there really isn't enough time to deal with any kind of justice to the subject, but i couldn't talking about fiscal policy not say some words about fiscal deficits. the congressional budget office estimates that the debt to gdp ratio, which was 40% at the end

11:17 am

of 2008, would go to 68% by 2019. but that bad news, bad bad news would only happen if a number of very implausible assumptions are made basically because of the rules that the cbo has to obey and making their forecasts. in coming to that conclusion that we will have fiscal deficit of about 3.5% and a debt to gdp ratio of 68%, they assume that all of the tax cuts that were enacted in 2001, 2003, and 2009 and that are formerly a sense of what the legislation says expected to win, they will end. and therefore tax rates will rise very substantially.

11:18 am

they also assume that there will be no real growth in discretionary spending. they don't assume that because doug elmendorf and his colleagues believe that. they do it because you have to have some rules and they want to have rules rather than judgment in the way that the cbo operate and the rules that they pick our whatever the law says the law says and you must grind out the implications of it. well, that's tax cuts, but they also tell us that if tax cuts were to be continued instead of ending as scheduled and that discretionary spending increased in line with gdp. well then the gdp to debt ratio would exceed 100% by 2009 team. another similar view of the fiscal problem comes from the ims which in the world economic outlook predicts that u.s.

11:19 am

fiscal deficit would continue after 2012 at about a 7% of gdp level. in other words, about twice the optimistic cbo numbers. well, what should be done about this? i think the challenge is to find a way to prevent the ever rising share of government spending and gdp. by 2019, the cbo numbers, the cbo numbers omnia assumption of no real discretionary spending are that we will be spending 23.6% of gdp with a more realistic assumption that government spending will rise to discretionary spending will rise with nominal gdp. we get to more than 25%. and to put that number in perspective, over the four decades through 2009 that number

11:20 am

was only a little over 20%. so with a five percentage point increase. and the danger in my judgment is that this will provide an excuse or provide political pressure to consider the value added tax and while value added tax is that many virtues as an alternative to other taxes, i don't think they have a virtue as simply an addition to personal income taxes, payroll pack the and corporate income taxes because they would increase marginal tax rate and encourage even more spending. so let me turn finally to the subject of the health insurance program. president obama has basically focused his energies on that program for expanding health insurance to low and moderate income households.

11:21 am

the 30 million people who would benefit we are told from the program will either be added to the medicaid rolls or will be given meaning and trent means tested subsidies to buy private insurance. so the major impact of all of this is a trillion dollar redistribution program aimed at increasing health insurance for about 10% of the public. and of course, the fact that it is mean tested, both the subsidies and the medicaid program, means that it will add to the usual adverse incentive effects of increasing implicit marginal tax rates. what concerns me more though is that the new law requires that insurance companies ignore preexisting conditions, preexisting medical conditions

11:22 am

in the availability and pricing of insurance. this is generally regarded as a great virtue of the legislation. i think it is a terrible problem of the legislation. why? physically what it says is that anyone can buy insurance at any time, regardless of the state of their health. what that does is to provide a very strong incentive for millions of middle income individual to drop their health insurance, to pay a small fine and that's what it would be and only buy insurance if they discover that they have some very expensive disease. typical policy for an individual cost something like $8000 figure for a family even more@@@@@@@ @

11:23 am

of course, it would make sense for individuals to buy insurance to cover the cost that might be incurred if they were in an automobile accident or had some other short-term spike in the health cost. something that they would not have time to get insurance for. but the major cause are things that individuals could prevent themselves. to individuals could present themselves to the insurance company for. so that i'm afraid is going to lead to millions of people facing the incentive to drop insurance. and the significant numbers of them take that, that will push up the cost of insurance for all the rest of s. who remain insured. if that occurs, congress will

11:24 am

have to completely revisit this legislation, completely revise the legislation, pushing us closer to publicly provided or publicly financed insurance for all. i don't know whether that's an intended effect of this or an inadvertent effect of it but i think it's a likely effect of it. but even without that, the medicaid expansion in the insurance subsidy in the senate and house bills will raise the national debt by nearly $1 trillion over the next decade. but of course, the spending part of this has been combined with a promise to increase taxes and to reduce medicare outlays so that the sandwich that is produced, spending increases and revenue sources, as far as the cbo's rules are concerned that they have to cost out to develop a whole. they tell you what the individual components are, but

11:25 am

the headline that comes out is that the legislation as a whole will not add a dime to the national debt indeed will reduce the national debt. but i wonder if anybody really believes that medicare outlays are going to be reduced by $500 billion over the next several years. after all, while getting ready to enact that provision, congress and of course that doesn't start for a few years, congress passed grade now been repealing previous legislation, which would have cut medicare payments to physicians by more than $200 billion. finally there's the issue of increasing health care costs. i think the obama administration and peter or his bag in particular have correctly identified increase in health care costs as a major problem

11:26 am

for families, for businesses and for the fiscal viability of medicare. and we know that the key cause of this rising health care costs is excessive insurance. and the administration and congress have recognized that in the proposal and the plan, at least in the senate version to increase the tax on or to remove the tax subsidy on so-called adalat health plans. in the end, they are focusing on taking away the tax subsidy only from a very small number of superexpensive plan. those are the only ones who will lose the tasks -- or a tax benefit. so there won't be any change in incentives. in said of a change in incentive they tend to power a committee of experts and call upon them to

11:27 am

report on the cost effectiveness of different health procedures. that's supposed to reduce cost significantly. but to do so without denying care or rationing care that patients want and are prepared to pay for through insurance. i think it is a technological approach to health care, an approach that ignores the fact that people have different preferences about health and health care. and therefore, differ in their willingness to spend on good i think that's unfortunate. thank you. caught [applause] >> first, let me say that i've managed the time poorly. and so, i'm renowned to the part where my paper will need to be cut back substantially.

11:28 am

and i can tell you in advance of the title in my paper -- the title of my paper is the federal reserve and the abatement of systemic risk and capital markets. now, actually i was first drawn to focus my attention on this other topic a long time ago. actually, i was a member of the board of governors of the fatter federal system in 1970. at that time, the present administration appealed to the federal reserve to provide assistance under which the subtle provisions of the federal reserve act, which allowed the federal reserve to provide direct credit to companies, industrialists, if they cannot

11:29 am

under the circumstances obtain funding from the commercial banks. the important theme at that time, there was no money left at the federal reserve bank who knew how to do this. so retirees were it so happens that the staff reported that a railroad company was not eligible because they did not have assets. the point is, the company was really fun being the major real estate project in florida with the use of commercial paper. at the end of -- they had millions of dollars of commercial paper.

11:30 am

we knew at the federal reserve that they could not roll them over. they would have to declare bankruptcy. then the question arose, what do we at the federal reserve do if we're not going to save them? i want to stress that. we do need to save the commercial paper market. three of us at the board tried to work out the principles under which the federal reserve would manage under these new circumstances. that is what we did. since that time, we provide to the reserve banks that they could provide the monetary restraint, but they would have to take the risk.

11:31 am

a risk of missing monies to the individual firms. so what principle did we work out that the board had to find circumstances, that the firm involved with the the segment of the market, which would be disrupted if they were under federal bank assistance. in other federal reserve has made use of that principle on a number of occasions. the most notable one, it was not directly at the federal reserve but at the treasury. during the mexican postwar, at the federal reserve collaboration with treasury used the exchange to legalization to provide support for the peso.

11:32 am

and the most important one, of course, in recent times was the long-term capital management. and finally, at the time the federal reserve issued a statement is that the federal reserve is a business and we will provide whatever assistance is necessary, regardless of the condition of the market, if the market is being threatened. but what i want to talk about today are the three most recent examples. these steel with vast earnings, lehman, and aig. now it just so happens that on

11:33 am

december 2, chairman bert mackie spoke to the economic club of washington and i was forcing it. i was invited to sit at the table, but edwards not several questions ahead of time and hope that i would have a chance to address these two chairmen bernanke. these questions were: the first the handling of bear stearns versus lehman. why did the federal reserve save bear stearns who made that decision? why was the decision made not to save lehman? who made that decision? what were the respective roles of the treasury, the federal reserve board, and the federal reserve bank of new york? why did the fed save american international, a group who made that decision?

11:34 am

why did the fed invest so much money in the project bikes first $85 million brought in to $85. and how would the federal reserve describes the ways into which the sharp expansion of the fed's balance sheet reflects its key role as a lender of last resort? now, we have done a lot of work on this issue before. and chairman bernanke answered those questions in that speech and subsequent answers provided to the congress. and they are all on the record. and i would leave those to you to read those. what i want to do just now is to focus on the question of, who should be the systemic risk

11:35 am

regulator in the future? the adverse proposers in the barney frank's bill, the chris dodd bill essentially in one way or another the federal reserve would roll in the management of systemic risk would be diminished substantially. my proposal is to do the reverse, but to make the federal reserve the anchor in a system of regulation and supervision. the question is not just regulation but also supervision. this is one of the powerpoint we would've made. what i have here -- you can't see this so i'll just describe. visualize your in a classroom, the students are not asleep, and the charts are on the board.

11:36 am

i have treasury, federal reserve, fdic and the sec. they are the principal federal government banks supplemented by the trade commission, investor protection act, and a new agency called consumer financial protection agency. basically, the federal reserve, based on its experience and using the principles i've just described, in which have been embedded in the system over the years would become the key consolidated resonator and the vice chairman had described these, chairman bernanke had described those as well. so that's the message of my paper. hopefully will have a chance to have a few discussion. now what i would like to do is

11:37 am

turn to to discuss these and ask them to make their comments. and after they make their comments i will not turn to the panel to form rebuttals but i would give the audience a chance to ask a question. so i will start in the book. jamie, margaret simms. >> how much time? >> five minutes. >> i had the somewhat challenging tax of delivering comments compared in real time and doing so in five minutes. so i will simply make a few remarks on each of the speakers as i heard them. vice chairman colin started his remarks by stating a principle to solve against adequate

11:38 am

collateral. it raises an important@@@@@ @ @ prohibited from a growing and not permitted to grow. as for fraud, restrictions on growth led to an early exposure and caused a collapse earlier this rather than later, a good thing because it limited the ultimate taxpayer losses. it is a personal question as to how you judge whether the institutions are solvent or not. you talked about the recovery of the financial markets. i want to ask the question as to whether it is fair to describe the institutions has recovered or not. stabilization of existing financial institutions -- and to

11:39 am

raise a delicate point -- it is not a goal in end of its self. i have no disagreement. i think it is a very realistic and bleak forecast for a slow and gradual recovery. realistic and a very bleak forecast for a slow and gradual recovery. i thought i very elegantly done. but the issue of course is whether a very gradual improvement is tolerable and is not what is to be done about it. and skip over a few things but i can't post on subjects without congratulating him in his final remarks invoking the spirit of making a crucial point that. the stability of the two instability and also for her, i think, making the point that monetary policy is a blunt instrument in this matter. as my old boss, henry burris coming is to say is what we need is the rifle shot of regulation,

11:40 am

not the blunderbuss of higher interest rates to deal with these questions. alan krueger stated the economy is not good enough albeit better than it would have then without the three pillars of financial stabilization, the housing program, and particularly the ara. those are all important but i would argue that they are perhaps even secondary to a fact or not gets mentioned on the panel, which is the effect of the overwhelming importance of the automatic stabilizers. we only live the stable issue that has occurred to the progressive income tax come into the social security system, to medicare into all the other apparatus of the welfare state that was given to us by woodrow wilson, franklin roosevelt, and winded and johnson. if it is preemptively before comment on the marks of professor feldstein. on the stress test, i have a different interpretation from secretary krueger.

11:41 am

i believe that they are best considered as a successful, highly successful public relations exercise. they led in effect to a case of engineered adverse selection, the signal was not the banks were solving, but that they were too big to fail and there is no question that the government can support the banks of it is determined to do so. it's not a question of having enough capital. banks do not lend capital to come back to kamensky is used to save eggs are not moneylenders they do not too have money in order to land. the issue is rather whether the financial structure that we are building through this stabilization program is one which is going to be effect to in producing a strong and rapid economic recovery going forward your alan krueger concluded by saying that we need to think in terms of rebuilding the economy. and what i would urge that given the stages in this crisis does is a very long-term proposition

11:42 am

which is going to require additional initiatives on a scale. so far not yet contemplated herein allen sinai pose the question what are the policies necessary to put the u.s. economy on a full employment price and financial stability while at the same time reducing federal budget deficits and debt relative to gdp? what i want to suggest is that maybe the case that there are no such policies. [laughter] absent a revival of housing crisis and a restoration of the financial wealth of the american public, which is non-prospect and a full reform of the financial sector which the administration has chosen to forgo. the private credit expansion which is the only known way to generate activity and tax revenues apart from direct government that reduces deficits inevitably won't occur. allen gives great weight, great authority to the power of these

11:43 am

monetary policies and stabilization. but i think i'm reading his paper, his was the only one i received in advance, that this seems to me to be an artifact of historical parameter values. interstate reductions cannot generate activity must they stimulate credit flows and of course we didn't get any credit flows. credit flows collapsed. what did happen was that kind of carry trade, reviving a staple at about that markets including the start market. this is a consequence and part of this. it is very difficult to see other support suspended. that is to say you have to believe in a very large wealth effect in order to believe that the quantitative easing ms. was responsible for an over 2% difference in gdp between 2009 in 2010. and what i was in fact saying in a simulation was that the quantitative easing prevented a further collapse of almost over 45% in the stock market, which seems to me to be possible,

11:44 am

something which is hard to know how much weight to give to that conclusion given how far do outside of the range of historical experience. okay, to come finally to professor feldstein, who is really in sharp contrast with allen sinai and his view of the matter. professor feldstein began his remarks with asset doubles broken monetary policy does not affe i have to say, we are in complete agreement on this point. i think this is the first time where i felt compelled to say we are in complete agreement. we are. i will differ with him on the question of the design of the -- i think that's in view of the

11:45 am

need for speed, the politically realistic thing was what was actually done. that was put together a bill. this is the way you got something done in a very short period of time. anything else would have been politically extremely difficult to accomplish. i also disagree with the professor on the substance of the matter. i think there was not enough aid and to protect public service jobs. the great weakness was that the continuing crisis means that the large part of the federal effort being offset by cutbacks. i will be there in just a second. the fact that these are low multiplier activities simply means that you must do more and

11:46 am

you can do more. but a larger number into the bill. -- put a larger number into the bill. hat we have scope for much larger effort to cut for this professor feldstein said the effects of it are small, relative to the 14 million unemployed. and finally, the danger now, it seems to be, a serious danger against which i wish to put you all on guard is that you pay too much attention to those who he says who are crying wolf about the dreadful prospect of a rising debt to gdp ratio as reported by this epo. this is just the least of our worries. these numbers are financial artifacts. if the private economy could do a major recovery they would go down. if they cant they will go up. either way the problem to focus on is that 14 million unemployed

11:47 am

or do nothing else the debt to gdp ratio goes up to greater than 100% by 2019. i have to say sold. in 1945 was 125% of the gdp. a father who was responsible for price price administration said a world war ii they share of responsibility for that and that led to the greatest period of american prosperity in modern history and that that can handle the public with a great source of the financial stability of the postwar american middle class. thank you. [applause] >> let me say to you that an article in the journal of the 1989 as i described this approach to just many in systemic risk. thank you, margaret. >> thank you.

11:48 am

i was asked to be on this panel when dr. rohmer was doing his paper on employment growth. so i was to speak to issues around employment and unemployment. at the most consistent statement in the five papers that were presented with that unemployment will continue to be a high. and i think that sort of day very weak land on which to hang a lot of comment. but on the other hand gives me a lot of freedom to say whatever i want to say. and i think that i would probably begin, since this is an evaluation, or supposed to be an evaluation of the first year of the obama administration policy is to say that there isn't a clear and cohesive employment policy. now it's certainly true that in the first year it's hard to articulate a complete and

11:49 am